XLC Communication Services SPDR June Outlook—Periphery industries firm up around Blue-Chips META, GOOG/L and NFLX

Price Action & Performance

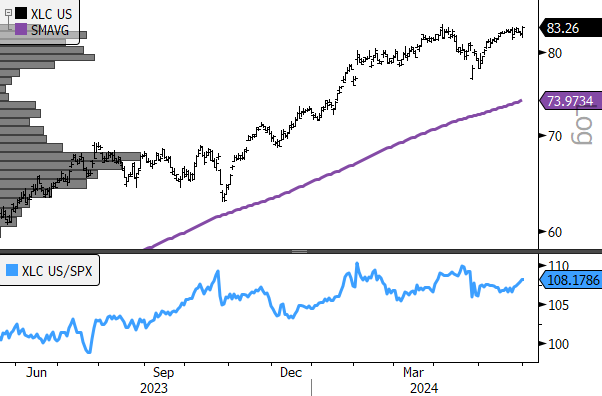

XLC has been a leading sector on performance over the past 12+ months since the market put in a trough in Q4 of 2022. Since then, XLC price has come close to its all-time high from late 2021 after buyers responded positively to a recent pull-back towards its 200-day moving average. The relative uptrend vs. the S&P 500 remains intact, and with periphery industries showing improving performance the sectors trajectory looks more sustainable. META’s advance to new all-time highs has taken a pause, and with the chart looking buyable, June will be a “tell” for the strength of the uptrend there. T and VZ are seeing positive momentum divergences over the intermediate term, as sellers may have reached exhaustion. NFLX continues to act well, and TMUS has a great month.

Economic and Policy Drivers

Alphabet Corp. (GOOG/L) and META are the two heavyweights in the sector. They are threatened somewhat by the prospect of rising rates, but more so by inflation manifesting high enough to raise recession probability which likely would cause correction as it historically coincides with major reductions in ad spending. So far, the inflation prints, and Fed. policy remain ambivalent, and investors are giving Growth stocks the benefit of the doubt in aggregate. It will be important to monitor the consumer as that is one area where fundamentals have been deteriorating in 2024. It’s one thing to talk about the CPI, but old and new media stocks that make up a broad swath of the Sector rely on advertising revenue. If the Consumer deteriorates any further, how long until the B2B space is impacted? That could end up a broad concern for internet adjacent stocks and keeps Fed. policy risk as a driver. In the meantime, election year ad loads are historically a tailwind to media co.’s and lower rates in the near-term offers a respite from a potential headwind that had started to chip away at valuations.

How Can XLC Help?

The Communication Services Sector is a collection of somewhat odd bedfellows as GOOG and META and a few other internet technology companies were merged with legacy Telco’s, print media and television concerns as well as various other entertainment properties and DIS. XLC provides an easy one-click way to manage exposure to all those various business lines. GOOG remains one of the strongest charts in the S&P 500 and NFLX looks great too. META is at a potential pivot which will likely be resolved when they report earnings. Meanwhile, with rates headed lower, the Sector includes VZ and T which have among the highest dividend yields in the S&P 500 universe.

In Conclusion

The XLC has improved steadily since the advent of the bull market in early 2023. Upside participation is broadening out and rates have failed below cycle highs for the 2nd time over the intermediate term alleviating that concern. The Elev8 Sector Model recommends an OVERWEIGHT position in XLC vs. the S&P 500 of +3.22% our largest overweight allocation for June

Chart | XLC Technicals

- XLC 12-month, daily price (200-day m.a. | Relative to SPX)

- XLC remains in an intact relative uptrend, with broadening industry level participation the sector remains is a top bet

Data sourced from Bloomberg